KPMG Australia's Ticking Debt Bomb

A$557 Million and Counting

Key Takeaways

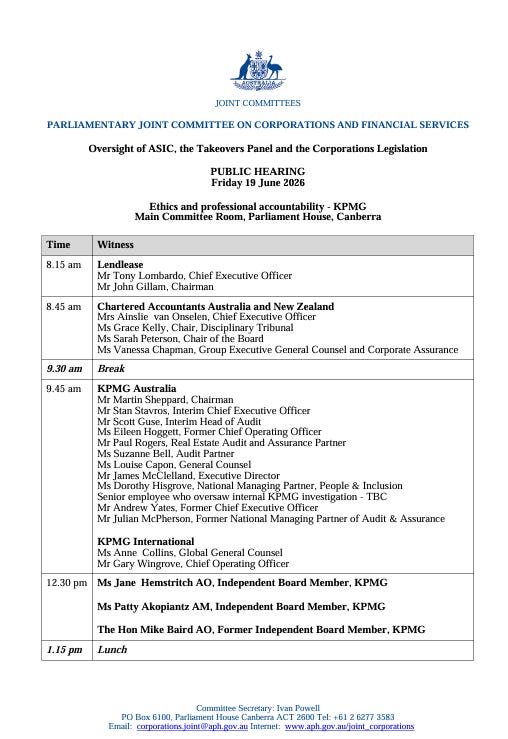

On Friday 19 June, more than 30 witnesses will appear before a parliamentary inquiry into allegations that KPMG partners misused confidential client information

KPMG Australia carries $557 million in debt (≈ $815,000 per partner) with revenue covenants, while revenue has declined from $2.553 billion (FY23) to $2.315 billion (FY25).

Major clients are reviewing or ending relationships, including Lendlease (~$10M), Westpac (~$32M), Macquarie Group (~$30M), and over $270 million in government contracts.

A covenant breach could lead to higher interest rates, stricter oversight, or partner capital calls — a deeper structural risk than the parliamentary hearing itself.

Tomorrow, more than 30 witnesses will appear before a parliamentary inquiry into KPMG Australia’s confidentiality breach scandal. Chaired by Labor Senator Deborah O’Neill, the Parliamentary Joint Committee on Corporations and Financial Services will hear from current chairman Martin Sheppard, interim CEO Stan Stavros, former CEO Andrew Yates, former Head of Audit Julian McPherson, former COO Eileen Hoggett, and independent board members — including former NSW Premier Mike Baird.

The hearing is expected to be intense, with sharp questioning likely over how the firm handled whistleblower complaints and whether confidential client information was misused to win new audit work.

The allegations, first raised by a whistleblower in 2024, centre on claims that senior KPMG partners improperly accessed and circulated highly confidential documents belonging to long-standing audit client Lendlease. These included competitor bids submitted by PwC and EY, as well as internal ranking sheets and other sensitive materials that were intended solely for Lendlease’s audit committee.

It is also alleged that during a meeting at KPMG’s Barangaroo office on 6 November 2023, a proposal was made for an internal audit partner to leave his laptop open with Dexus internal audit documents visible while he went for lunch, so that external audit personnel could view them.

According to the whistleblower, this confidential information was relayed to the firm’s tender war room, where it was used to strengthen bids to win the external audit mandates for Westpac and Dexus.

KPMG Australia is under considerable pressure. Its reputation has been damaged by the allegations, long-standing clients are reviewing or terminating relationships, and a material share of government contracts faces review. These issues are serious, yet the firm’s approximately $557 million in borrowings — and the revenue covenants attached to them — may represent a broader structural risk.

Why KPMG Australia Had to Borrow So Much Money

One of the key reasons KPMG Australia has borrowed $557 million from National Australia Bank (NAB) and DBS lies in how professional services partnerships traditionally operate. These firms typically distribute the vast majority of their profits to partners each year rather than retaining earnings to build a financial buffer or “war chest” for tougher times.

Because profits are calculated on an accrual basis — meaning revenue is recognised when work is delivered, not when cash is received — the firm can report strong profits on paper long before it has even invoiced the client, let alone received payment.

In such situations, the only way to fund day-to-day operations — including salaries, rent, and other running costs — is to borrow heavily.

This approach was addressed during a 2023 parliamentary inquiry, when then-CEO Andrew Yates was questioned by Senator Barbara Pocock about the firm’s growing borrowings. Yates stated:

“We borrow to fund the operations of our firm, which generate profit… We don’t borrow money to then directly distribute that money to partners.”

While technically correct in a narrow sense, the reality is that the debt was necessary to enable the firm’s high level of profit distributions. Without it, KPMG would not have been able to maintain both its operations and its partner payouts at the same time.

Why the Covenants Are a Problem

The loan agreements include revenue covenants, which require the firm to maintain minimum levels of revenue.

These terms were negotiated when KPMG revenues were growing at a steady rate. However, since the PwC scandal in 2023, KPMG’s revenue has declined:

FY23: Record high of $2.553 billion

FY24: Sharp drop of 6.5% to $2.386 billion

FY25: Further decline of 3.0% to $2.315 billion

This pre-existing weakness has left the firm with much less headroom. Any significant further drop in revenue now risks pushing it into breach of its banking covenants.

Client Relationships Under Pressure

Several major clients are actively reviewing or have signalled they will end their relationships with KPMG Australia, with the largest potential losses concentrated in audit work.

Long-standing client Lendlease has effectively ended its audit engagement, worth approximately $10 million annually.

Westpac’s audit mandate, valued at around $32 million per year, is under active review and faces possible termination.

Macquarie Group’s Australian audit work, estimated at roughly $30 million, is also under scrutiny.

Dexus is expected to review its audit relationship with the firm.

On the government side, KPMG holds federal contracts worth a combined $653 million, of which more than $270 million is already under review.

Taken together, these developments represent a significant revenue exposure across both audit and consulting.

What Happens If the Covenants Are Breached?

A breach of the revenue covenants would give the lenders material rights under the loan agreements. While an immediate acceleration of the full $557 million debt is considered unlikely, the banks would have several levers available to them.

These could include increasing interest rates, requiring additional security or guarantees, imposing stricter reporting and oversight, or declining to renew facilities on maturity.

For a professional services firm that relies on debt to manage working capital and partner distributions, any of these measures would create meaningful operational and liquidity pressures.

The Impact on Partners

The consequences would not be limited to the firm itself. Because KPMG Australia operates as a partnership, the structure can expose partners to financial consequences if the firm’s position deteriorates materially.

With roughly $815,000 of debt attributed to each partner, a serious deterioration in the firm’s financial position could result in partners being asked to inject personal capital to support or repay the borrowings.

For some partners, particularly more junior ones, this could create significant personal financial pressure.

The fact that many partners already structure their personal affairs (such as holding the family home in a spouse’s name) to protect against this kind of liability underscores how real the risk is perceived to be within the firm.

KPMG International has reportedly blocked further partner exits both to ensure the firm retains enough partners to meet its client commitments and to prevent large capital repayments to departing partners at a time of financial stress. As a result, many partners now have no straightforward way to exit before potentially being asked to contribute personal capital.

The Reckoning Ahead

While tomorrow’s hearing will attract intense political and media attention, the firm’s financial structure — its $557 million in borrowings, the associated revenue covenants, and exposure to major client losses — represents a deeper challenge.

Hundreds of partners and thousands of employees have their careers and financial interests tied to KPMG Australia. The vast majority played no role in the issues under scrutiny.

It is notable that Andrew Yates, the former CEO during whose tenure these issues emerged, is understood to be leaving with a substantial exit package, while many remaining partners could face requests to contribute personal capital if the firm requires additional support.

The coming months will test whether KPMG Australia can retain key clients and manage its banking relationships successfully. The combination of reputational damage and high financial leverage creates a challenging environment, and the firm’s ability to navigate these pressures without further disruption remains to be seen.